June 17:

Source: seekingalpha.com/article/3261745-chevron-under-100-is-a-steal

Summary

- Few oil majors are better at deep water exploration than Chevron. Offshore drilling will grow from here as onshore plays have all but been exhausted. Chevron is well positioned here.

- When Chevron committed to Gorgon, it did so when oil prices were in the $60s. This project (and Wheatstone) will be highly profitable for the company and will boost cash flow.

- The price-to-book ratio has rarely been cheaper and the dividend has increased to 4.31%. Natural gas is the future as coal plants worldwide generally are declining on a historical basis.

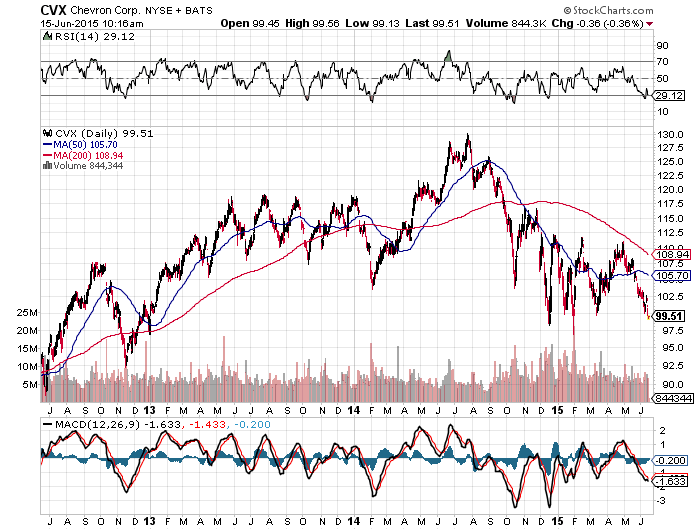

At the time of writing this, Chevron (NYSE:CVX) was trading at $99.49 -- an 11% decline year to date. The chart below shows that it looks to have support around these levels. Only time will tell if it will hold up. What is very apparent is how the Greek situation is affecting the euro. If the Greek situation deteriorates more from here, the dollar will rally against the euro, which will put pressure on oil and other commodities. Probably more than other integrated oil majors, Chevron needs a rising oil price as its upstream division is substantially bigger relative to its downstream. Furthermore, most of its producing upstream is in liquids, not natural gas -- 66% of its business is in liquids vs. 48% at Shell (NYSE:RDS.A) and 51% at Exxon (NYSE:XOM).

This served Chevron well in the past as liquid production is generally more profitable than natural gas (in a rising market), and oil prices up to 2014 were much higher -- resulting in generous company profits. However, profits have deteriorated over the last few quarters and the company is finding it difficult to finance all of its operations. Therefore, in order to finish off current products (Gorgon, Wheatstone, "Big Foot," etc.), the company has cancelled its share buyback scheme this year in order to preserve cash.

Furthermore, the company has aggressively begun to cut costs (both with suppliers and in-house), and stated that it will sell $15 billion of assets through 2017. Also, $6 billion of debt has been issued this year to meet capex and shareholder commitments. The objective here is that the company gets its most imminent projects to production as quickly as possible and then hopefully the price of oil and gas cooperates. However, in my opinion, Chevron has other distinct advantages that some of its peers don't have. Lets go through them.

(click to enlarge)

First, the onshore shale fracking boom in the U.S. has resulted in 70% more oil and gas produced in 2014 than the country produced in 2009. The U.S. now is nearly producing the same amount of oil and gas as Saudi Arabia, which is unprecedented. Many analysts are now predicting that the U.S. will finally lift the ban on crude exports, which has been in operation for the last 40 years. Although the U.S. is saying that there are at least 50 billion more barrels of oil available (14 additional years of current production) from its shale formations, shale plays can be tricky because the decline rates are large. For diversification purposes, big oil majors also go offshore to avoid the unpredictability shale plays provide.

Its one thing having a shale play full of oil and gas, but another extracting the energy profitably. The future will be offshore as the plays are generally far bigger and more reliable once the platforms are in position. Chevron in this area has few competitors. The company has years of experience in successful deep water exploration and production, which should definitely add value to the company going forward.

One of its current offshore projects is called "Big Foot," which is a Gulf project 220 miles south of New Orleans. I was surprised to learn that nine of the 16 anchoring tendons lost buoyancy recently. In a way, it was better that this happened now and not when the company was far closer to production, which would have increased the risk of platform damage. Chevron is continuing its investigation into the matter and I have no doubt it will learn from it. Production of 75,000 barrels of oil per day will be delayed until 2016, which is a minor issue in the grand scheme of things. The crucial issue is that "Big Foot" becomes a success ,which should bring more offshore opportunities to Chevron down the line.

The second advantage Chevron has over its peers is the strategic position of its Gorgon and Wheatstone projects in Australia. As outlined above, the U.S. has never had so much oil and gas, but Australia -- and, more specifically, the Far East -- is a different story. An ever-increasing middle class in Asia will definitely be energy hungry in the next few years, and natural gas will be the answer.

Gorgon and Wheatstone ($84 billion+ investment to date) will produce 4 billion cubic feet of natural gas per day. This energy will primarily supply Japan and the Far East. I acknowledge that there has been massive cost overruns on the Gorgon project in particular, but investors have to see he big picture here. Gorgon, for example, will provide natural gas for an estimated 40 years. Now, when Chevron committed to gorgon back in 2009, oil prices were in the $60s. This leads me to believe that current energy prices (even though well down compared to 12 months ago) won't really affect the long-term profitability of this LNG project. Chevron might be troubled by cash flow at the moment, but once these huge projects come on stream, healthy profit margins will flow again.

Finally, let's discuss some numbers. Chevron's production target is 3.1 mm boed (millions of barrels of oil equivalent per day) by 2017. Currently, it is producing approximately 2.6 mm boed. That's a 20% increase from current levels. Chevron (although hurting in the short term) has a long-term view of its business. It has doubled down on production because it believes natural gas will be the energy of the future. Renewables are not ready yet to take the place of coal on a global stage, but clean natural gas will surpass coal in many markets in the next few decades. Chevron will be at the forefront and even more so if offshore investment accelerates.

With a current yield of 4.31% and a present price-to-book ratio of 1.2 (10-year lows), this stock has never been cheaper. I, for one, believe there always will be a floor under energy prices. As prosperity on a per capita basis increases in the world, energy demands will be higher. I believe Chevron will easily rally 20% from here as production levels increase and energy prices gradually drift higher. I'm long Chevron from here.

Source: seekingalpha.com/article/3261745-chevron-under-100-is-a-steal

Comments

Post a Comment