June 15:

Source: seekingalpha.com/article/3260295-baker-hughes-overvalued-but-supported-by-the-pending-deal?source=partner_newsnow

Summary

- Baker Hughes exposes the investor to moderate-high risks, with profitability a major concern.

- 30% of the current market price is attributable to a premium for Baker’s future growth.

- Yet margin of safety is negative, with terrible medium-term prospects.

- Majority of Wall Street analysts believe this is a buy.

- But such opinions likely stem from the still-pending, shareholder-approved merger with Halliburton.

Continuing off from our assessment of Halliburton last week, we evaluated the investment worthiness of Baker Hughes Inc. (NYSE: BHI) as a standalone stock, as we are interested in seeing how it appears from a margin of safety perspective.

However, our analysis and valuation call out BHI not only as a moderate-high risk company, but also as an overvalued stock that, had it not been for its merger with HAL, might have seen worse times. While it is possible the merger may be renegotiated to a valuation lower than the initial deal value of $35.3 billion ($38.5 billion in enterprise value), we know nothing about the deal status other than management's favorable commentary in its most recent earnings call back in April, in addition to the intention to shed off $3.5 billion in annual revenues post-combination… of course to appease anti-trust regulators.

Risk Assessment:

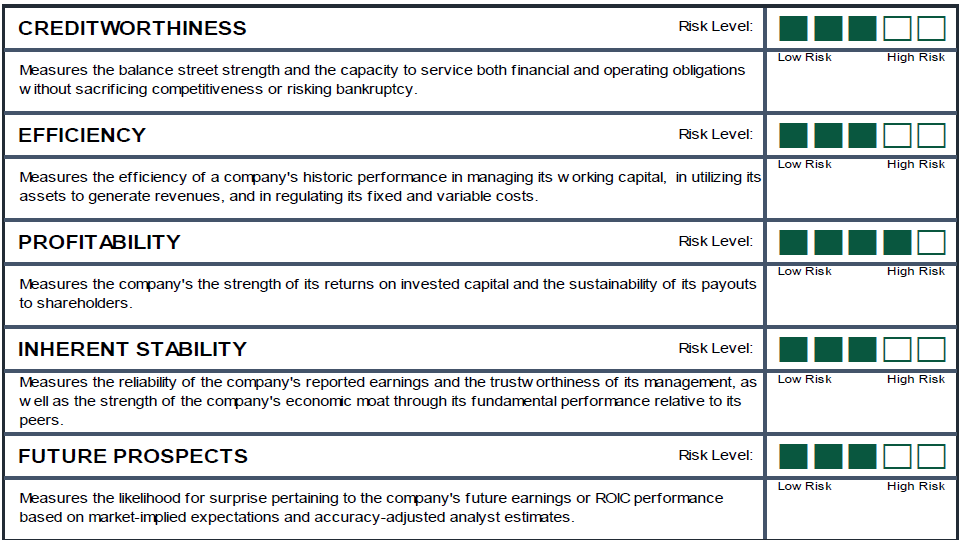

We evaluated Baker Hughes using a systematic, rule-based risk assessment method. It is a balanced scorecard that considers the past performance, historical volatility, and underlying trend of over 40 different risk factors in multiple factor groups and utilizes proprietary standards to systematically score these risk factors across five levels. We believe such analysis adds value for the reader, as they adequately define the major risks in any business, accurately measure them, and succinctly describe them in an easily comprehensible format.

(click to enlarge)

Source: Saibus Research

While our risk measurement process rated Baker Hughes as "moderate" for four of the Five Elements, because of the varying weights we apply to our risk factors, BHI's score is actually borderline moderate-high, largely due to the level of risk arising from the company's profitability. In this article we will discuss this, as well as BHI's Future Prospects, seeing as how the oil markets are still in a state of heavy flux.

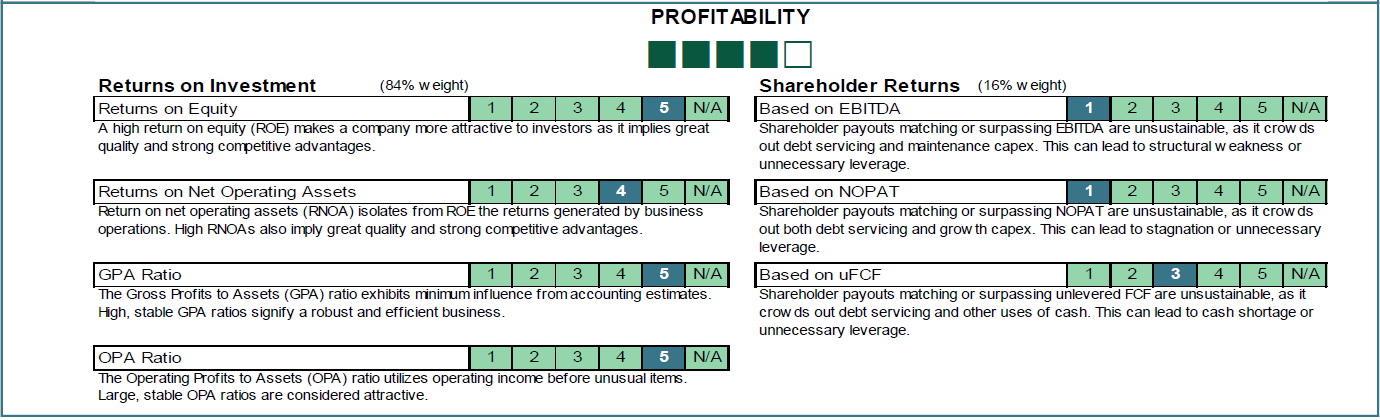

Now, when we discuss profitability, we refer strictly to returns on invested capital and the sustainability of a company's shareholder payouts (dividends and buybacks). We do not discuss profitability margins under this section as these are ultimately another factor of returns on investment. Whether margins or sales volume are given more weight depend on the company's underlying industry, its business model, and its ability to control its costs.

(click to enlarge)

Source: Saibus Research

Returns on investment reflect the ultimate performance by the management team. Various metrics are used to assess the attractiveness of BHI's business, the strength of its core operations, and the soundness of management's decisions to return money to shareholders.

Baker Hughes's returns on invested capital have become atrocious after 2008. ROE fell from its cushy 20+% levels to the mid-single digits, while RNOA collapsed from an excellent, competition-beating 30+% to the mid-teens, the realm of mediocrity.

(click to enlarge)

Source: Saibus Research

Furthermore, decomposing the operating segment of ROE (via RNOA) shows us that ongoing operations have supplied and are still supplying more than 100% of Baker's returns on investment, indicating that the low debt ratios still dragged the company down.

(click to enlarge)

Source: Thomson Reuters, Saibus Research

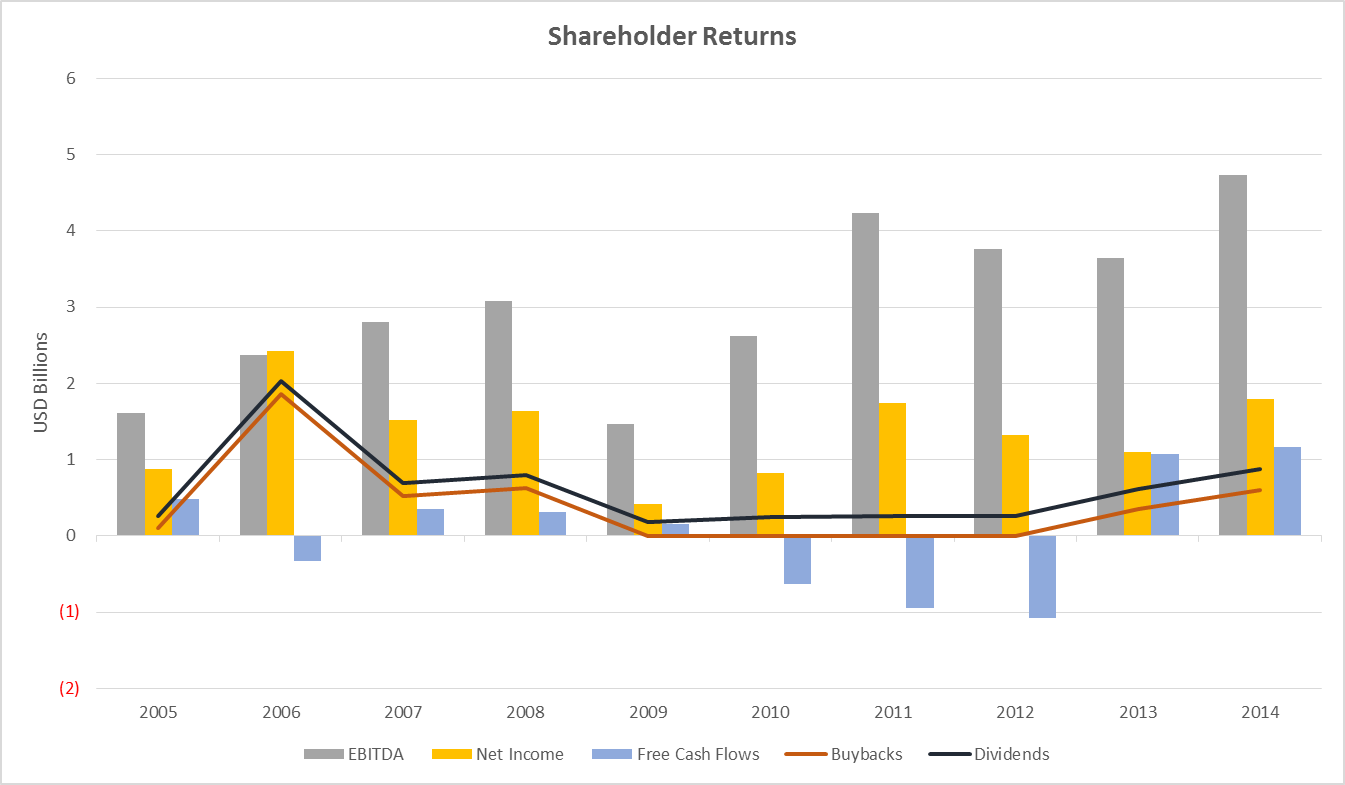

Cumulatively, shareholder payouts totaled $6.2 billion over the last ten years, compared to $13.6 billion in net income. If we were to adjust our time frame to start with 2007 though, we saw that more than half of this came from 2006, as 2007 - 2014 totaled $3.9 billion in shareholder payouts, compared to $10.34 billion in net income.

It appears that the company looks like it's behaving conservatively with respect to its earnings power, though the reliance on debt financing (given its low levels of free cash flows) to pay off dividends and buybacks probably perpetuated a portion of the company's financial obligations.

However, BHI's share repurchases have not added much value to investors, as there were no net decreases in shares outstanding over time.

Much of the company's high risk profile for the profitability element comes straight from the worrying ROICs, and it looks like we shouldn't expect too much improvement on that end. Not for a while.

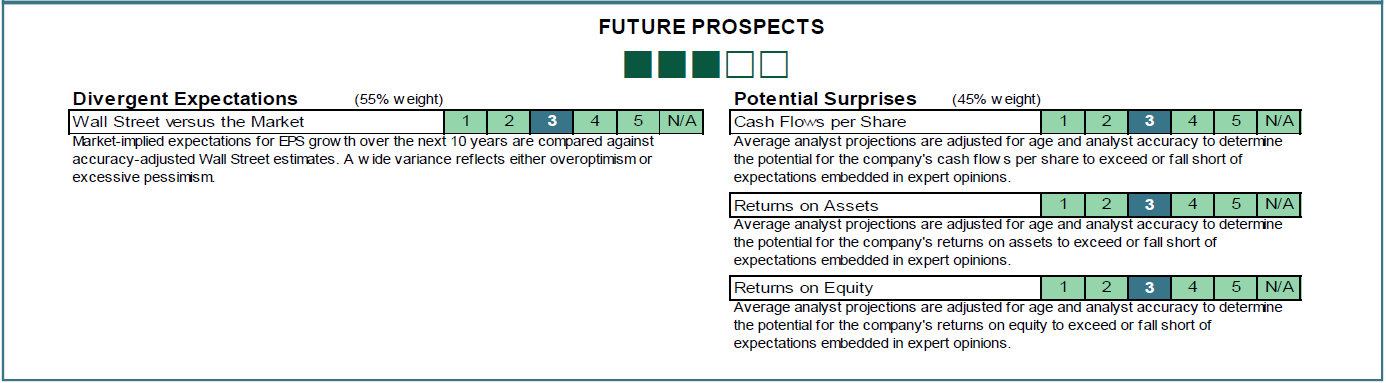

Moving on to future prospects, we consider this element from two perspectives. First, we considered the possibility the company may surprise Wall Street's expectations for cash flow per share, returns on assets, and returns on equity over the next three fiscal years. Second, we contrasted Wall Street's forward 10Y EPS growth projections against the market-implied expectation of same, if the data is available.

(click to enlarge)

Source: Saibus Research

Although this cannot completely substitute for true industry research, which relay the qualitative trends and developments noted by technical and economic experts in an industry, and a thorough, qualitative perusal of the firm's strategic focus and adherence to its organizational values, appraising the detailed expectations set by Wall Street's sell-side research allows us to grasp the future prospect of the company by proxy.

The table below details Reuters' compilation of analyst estimates (after adjusting them for the analysts' track record and level of experience) for Baker's financial performance, looking ahead over the next three fiscal years.

Source: Thomson Reuters. Analyst estimates for revenues and degree of profitability were also included for clarity.

With more than 50% of Baker's top-line historically and currently dependent on the United States, undoubtedly this would suffer the most as OPEC aggressively fights for market share, even if it meant exacerbating the existing oversupply. A 34% drop followed by unimpressive growth. Overall, an 8% compounded annual rate of decline through the next three years.

Additionally, profitability itself is expected to decline as the marginsthemselves plummet, cut in half. Our valuation analysis assumes mean reversion back to the mid-teens, but then again, the time frame does not do BHI's stock any favors.

With ROA and ROE down and capital expenditures still elevated despite the setbacks coming from the top-line, the company is just as likely to ramp up leverage, perhaps beyond than what is implied by the estimates in the table above.

Not exactly a good portrait of the future.

Valuation Analysis:

Proceeding forward, we ran our valuation analysis using a risk-adjusted WACC of 9.61%, a terminal growth rate equal to 1.56% in long-term inflation (United States), average free cash flow margins of 6.24%, which reflects a 32.6% tax rate, net investments close to 0% (i.e. capex equals depreciation), and operating margins of 13.3% (the 7Y moving average) by 2020, clawing back up from the expected 2% for FY 2015. We also use a competitive advantage period of 9 years to account for the moderate riskiness of BHI's economic moat.

Enterprise values as computed are subject to a negative $4.8 billion adjustment that accounts for non-operating cash, debt, and dilution, as well as other extraneous factors like deferred tax liabilities. This overall adjustment corresponds to -$11 per share, but the firm's debt can be broken down to $9.5 per share, thus signifying the impact of financial leverage on equity value. We did not factor in BHI's share repurchases as they did not add value to investors.

(click to enlarge)

Source: Saibus Research

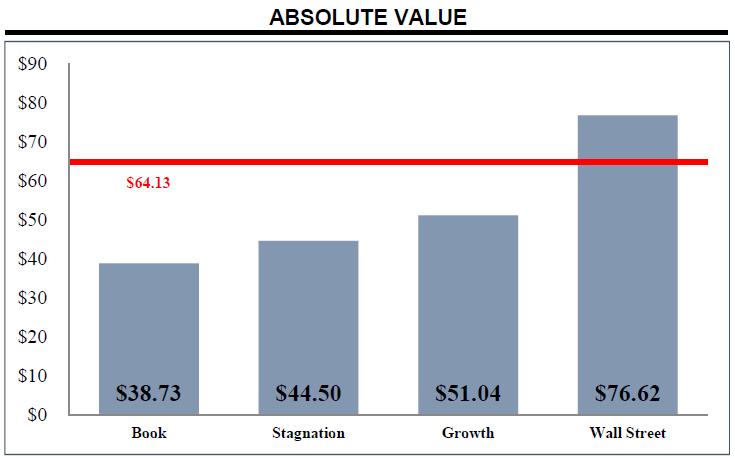

In a steady state scenario, we presumed sales to instantly decline 16% to $20.5 billion from its FY 2014 value and stay there, with profit margins steady at 7.6% (calculated with an 11.3% operating margin and the same tax rate mentioned earlier). Capitalizing the profits and adjusting them will yield a $19.3 billion equity value, or $44.50 per share.

In a growth scenario, using the conservative assumptions as defined above, we further presumed a conservative CAGR sales growth of 13.06% in the years after FY 2017. This produces implicit compounded annual growth estimates of 5.6% and 8.8% per year for sales and unlevered free cash flows, respectively. However, we caution that the ability for BHI to meet these expectations depends on what it does to survive the duration of the downturn. Nevertheless,the result is an equity value of $22.2 billion, or $51.04 per share.

Before we move on, we'd like to point out that BHI closed at $64.13 per share last Friday, the 12th.

The gap between Net Assets and Stagnation implies that Baker's assets are responsible for 87% of its sustainable earnings power. This reflects negatively on BHI's economic moat, as it suggests weakened or shallow competitive advantages. However, should the BHI-HAL merger push through, we expect no more than $7.5 billion in assets ($17.25 per share) and $3.5 billion in revenues ($9.47 per share in stagnation value) to go away, which - after doing the math - indicates Halliburton had identified and has plans to strip off businesses in which BHI's economic moat did not add much value.

Comparing Stagnation to the market price produces a $20 difference. We interpret this to mean that 30% of Baker's market price contains a premium that investors pay for Baker's future growth. As the fundamentals and future prospects don't appear to justify this premium, it is likely that this is coming from the synthetic put option created by the pending merger.

Margin of safety also does not exist with BHI, not against our estimate of intrinsic value. In other words, our estimates imply an overvalued business. If we happen to be wrong and Wall Street consensus was correct, the latter's target price of $76.62 represents a 16.3% margin of safety at the current price, or a potential upside of 20%. But even then, is this margin of safety acceptable?

With the level of risk inherent in BHI, we don't think so. Not as a standalone investment.

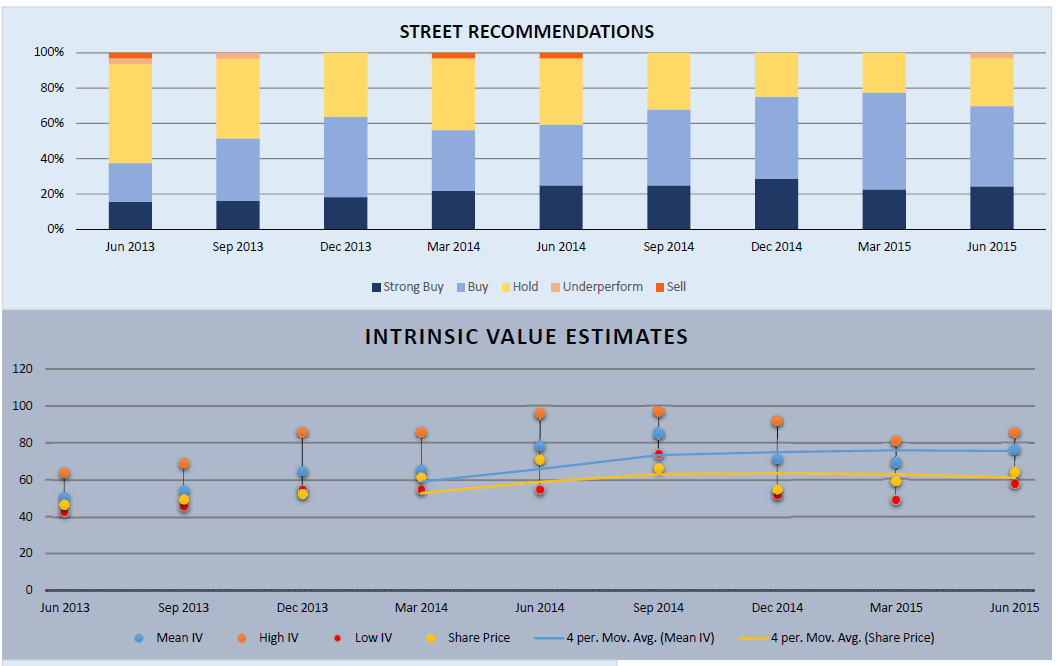

We note that 31 analysts from large financial institutions currently follow BHI. These people see value in the company's stock and most are currently recommending a buy.

(click to enlarge)

Source: Thomson Reuters, Presentation by Saibus Research

However, as we stated before, we believe the reason why these analysts are still positive about BHI's stock and why the market price remains elevated at $64 despite the market downturn falls on the pending BHI-HAL merger.

Most BHI and HAL followers already know the details. On November 14, 2014, Halliburton announced a stock swap transaction to acquire Baker Hughes by offering $19 in cash and 1.12 shares for every share of BHI. HAL closed at $55.08 per share on the announcement date, implying that BHI was worth $80.69 per share - a $35 billion deal.

Under the current market prices, with HAL closing at $45.48 last Friday, this suggests BHI is worth $69.94 assuming the merger happens the way it currently stands. A deal worth $30 billion. BHI's current price has a 10% return built into it, provided that both HAL and BHI do not fall any further. If the deal remains at $35 billion, then HAL shareholders would suffer as management must dilute them by another$5 billion to meet the announced deal value.

Source: seekingalpha.com/article/3260295-baker-hughes-overvalued-but-supported-by-the-pending-deal?source=partner_newsnow

Comments

Post a Comment