May 06:

Summary

- Prior analysis of the Tesla battery pack offerings neglected to simulate actual usage leading to unsubstantiated conclusions.

- A physics-based analysis of the battery is presented in the raw as are unbiased results from multiple simulations.

- Investors should use these results to gain insight to the economics of the battery business so that the future hurdles and business decisions that Tesla faces become clear.

Several articles on this site have weighed the significance of Tesla's (NASDAQ:TSLA) battery offerings and whether they make sense from the perspective of a consumer. I intend to add to this discourse by contributing robust calculated results from my own proprietary code and present an unbiased numbers-driven analysis of the economics of battery assisted solar power.

Background

My previous article looked at a few quick and dirty back of the envelope calculations to figure out when and where solar would reach parity with the grid and I was surprised to find that it already had in virtually all markets. This led me to develop a much more robust way of figuring out if solar made sense for individual homeowners to mine for a potential business case. The following calculations focus on a particular representative market in the southeastern United States where most customers receive power from the Southern Company (NYSE:SO). There are no available net metering programs and much of the electric bill is fixed, subsidizing various projects including nuclear power.

Almost all customers in this market use natural gas for heating during the winter, which substantially lowers their electrical usage during those months. Furthermore, electrical usage is tiered incrementally so a heavy user pays less per kWh in the winter and more per kWh in the summer than light users. Location-specific data for electrical usage and meteorological data including the incident solar radiation is pulled from the database provided by the National Renewable Energy Laboratory. The database conveniently overlays data for weather and electrical usage by the hour for several locations during their test year.

Calculations are based on every variable I could find in the literature from the location of the sun in the sky over the year to the efficiency of the panels as a function of temperature to the performance of the inverter. Readers should treat these calculations as robust and any assumptions not driven by physics will be explicitly noted. Pricing is based on extensive business planning and should also be treated as robust. The only pricing number fudged due to the timing of this article is an inclusive $1000 installation and delivery cost for the Tesla 7 kWh battery pack. The calculations assume that the provider will buy the Tesla pack directly and install it in homes with a solar system that includes an inverter. SolarCity's (NASDAQ:SCTY) current offerings are not associated with any calculations performed, but their competitive stance should be considered to be somewhat worse than the base cases I use here.

No Battery Case

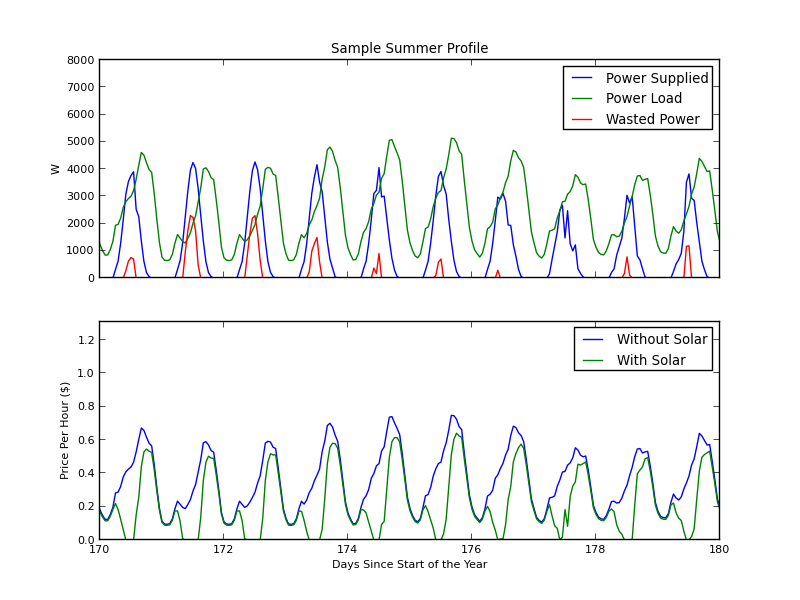

I thought a good metric for the economics of solar and solar batteries would be the annualized rate of return on investment. That is, over the life of the system, the equivalent rate of return a customer would get on the money they spent on the system in energy costs saved. A positive ROI implies that the system at least paid for itself. I ignored intangibles like the equity of the home and assumed an average 3% yearly increase in utility costs. The best-case scenario for the representative customer is a 5.7 kW system.

(click to enlarge)

Source of all images: Author's work

Calculations show a ROI of 2.16% per year for the warrantied panel life of 25 years with an average cost of 10.86 cents/kWh for captured solar. Due to the absence of net metering, much of the energy produced during midday is wasted even during the winter, but using less grid energy overall brought the customer down to a lower summer pricing tier.

Battery Case

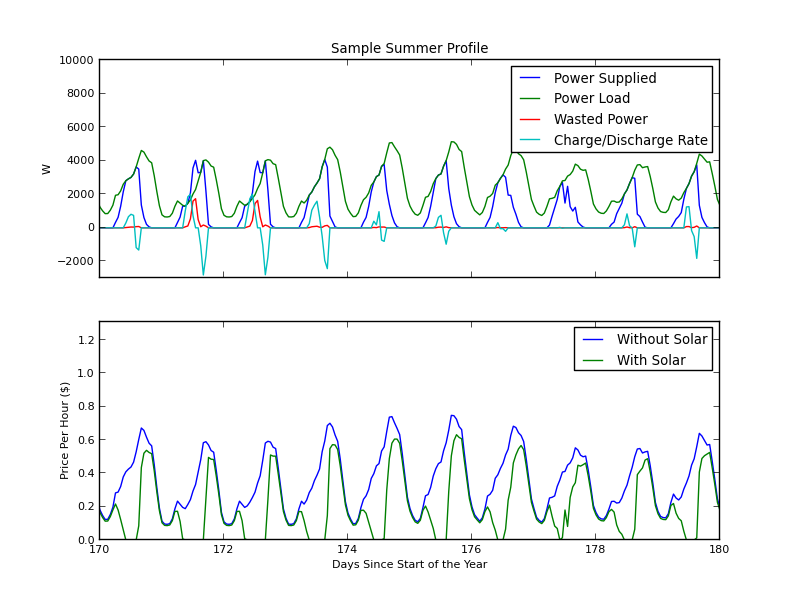

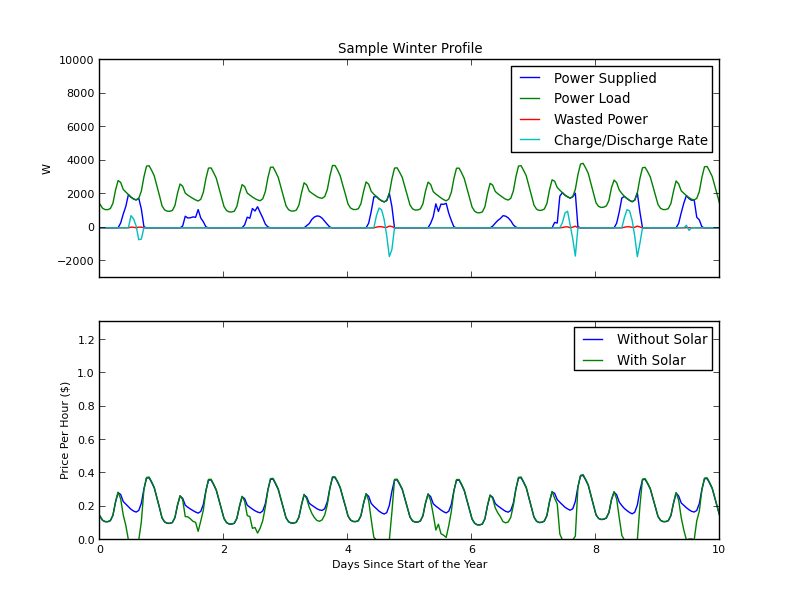

One of first, most important results of the battery calculations is that one day is not the same as one cycle. If one were to simply add a 7 KWh pack to the panels in the previous case, the batteries would only cycle around 2000 times through the 25 years. Without data from Tesla, calculations assumed that the batteries cycle between 10 and 90% of the maximum depth of discharge to preserve their life and that their cells retain 80% of their initial capacity after 3000 cycles, decaying exponentially.

The degradation rate is the subject of much debate so I should emphasize that while I do believe this aligns with results from the Model S battery pack, even assuming 1000 cycles to 80% does not change the premise or the conclusions of this article. Provided are three charts showing the key metrics for a customer with a 5.7 kW system and a 7 kWh battery pack from Tesla.

(click to enlarge)

(click to enlarge)

(click to enlarge)

The ROI for the best case using a Tesla battery was 1.36% per year with an average cost of 12.84 cents/kWh for the combined system.

The calculations address some other key points of consternation between detractors and supporters of Tesla's battery. The maximum energy usage rate at any time over the entire year was 7.2 kW for those sizing the needed number of batteries. Secondly, there was no way to cover all energy needs off the grid with a positive ROI or less than 10 batteries.

Goals for Economic Feasibility

Elon Musk justified his battery launch by lauding its potential as a backup for power outages, a companion for solar power, and for load-balancing.

As a backup source, customers should not expect to go on about their life as if nothing happened in the event of a massive storm crippling the grid for days. Coupled with solar and using energy sparingly for the essentials, it could make such an experience a bit more manageable however. With some energy use planning, short outages would be well managed by the system in low demand periods. For that reason, a solar customer in the case outlined above may find that added utility worth the small hit to the ROI.

For solar customers unfazed by power outages, the battery is a bit too expensive to fully justify purchasing one in markets with cheap electricity. For markets with expensive electricity where solar panels have higher margins, batteries and panels converge in price. In order to fully recognize the scale of the gigafactory, Tesla would need to drop the price of their batteries so that they are more broadly competitive.

A 30-50% drop in price would correspond to a massive broadening of their addressable market and investors should treat such an announcement as a play for an aggressive expansion of their battery business.

Additional disclosure: Tesla will rise or fall on its fundamentals. I do not seek to introduce any bias into my articles. I only seek to inform and analyze.

Source: http://seekingalpha.com/article/3147816-full-simulation-of-the-tesla-battery-insights-for-investors

Comments

Post a Comment